The Single Point of Failure

The market just bet your retirement on a story. Here is how a steward builds on something the story cannot touch.

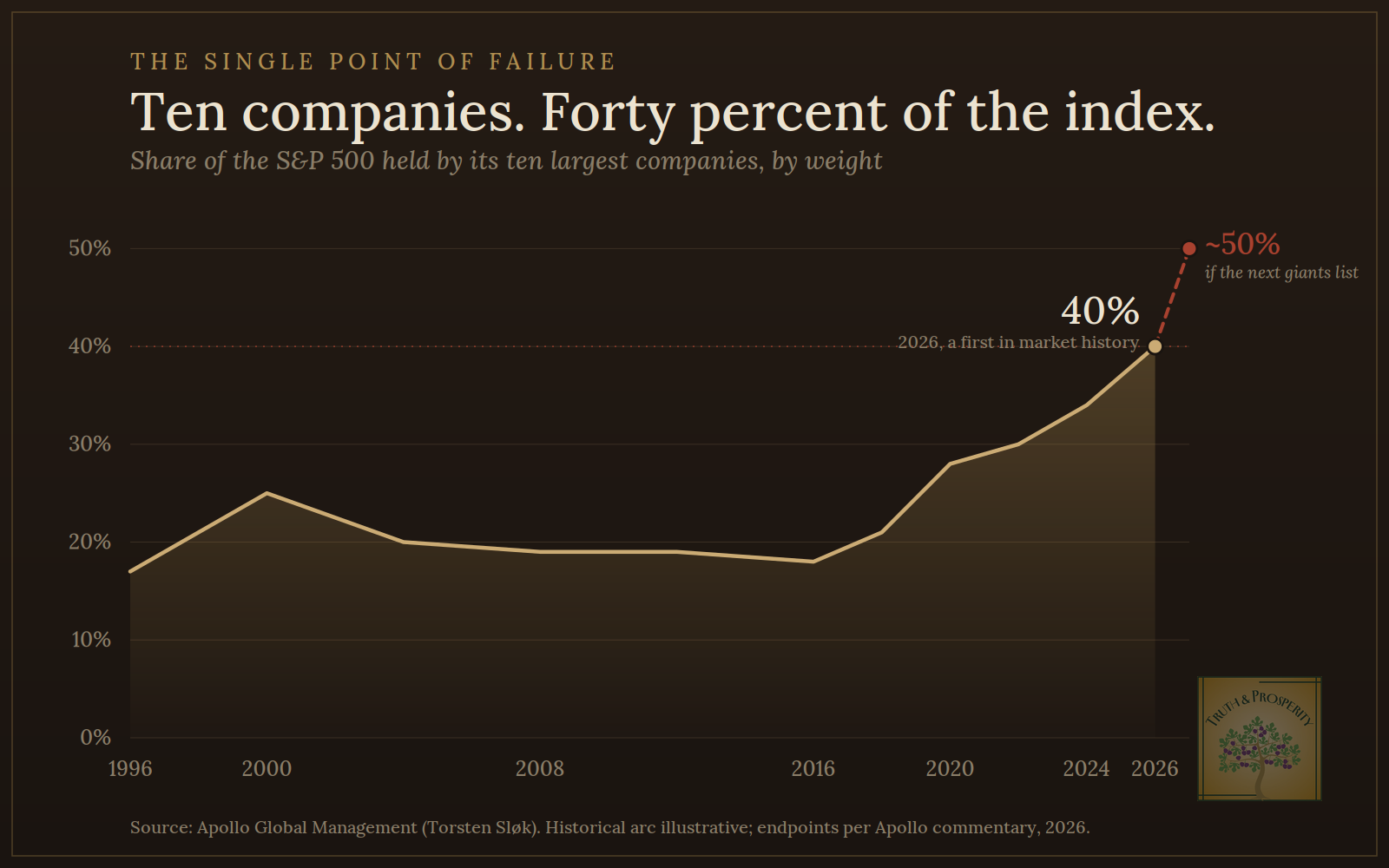

For the first time in the history of the American market, ten companies are now worth more than forty percent of the entire S&P 500.

Five hundred companies in the index.

Ten of them hold forty percent of the weight.

Nearly all of the ten are riding the same story, the same two letters, the same promise that has been printed on every magazine cover and shouted from every cable desk for two years straight.

Torsten Sløk, the chief economist at Apollo, has a name for what this is. He calls it a single point of failure.

He is one of several serious voices, alongside Michael Burry and the Man Group, pointing at the same thing.

The index your 401(k) tracks, the one your advisor told you was diversified, is no longer diversified in any meaningful sense. It is a concentrated bet on a handful of firms and one narrative. And Sløk’s own firm notes that if a few more of these private giants list this year, that concentration could climb toward half the entire index.

You did what you were told.

You bought the index fund.

You set it and forgot it.

And while you were not looking, the men who manage the money quietly turned your retirement into a wager on a single story, “AI.”

However, I don’t want to write an article about that story. This is an article about you.

A Word Before the Teardown

I am not a guru, and I am not here to tell you to sell everything and bury cash in the yard. I have spent decades as a chief financial officer, building organizations that had to actually work, signing the front of paychecks and not just the back. I know how to read a balance sheet, and I know how to build things that do not fall over.

I will also tell you plainly: I use these tools every day. The large language models, the ones the headlines insist on calling something grander, are genuinely useful. They check my grammar. They organize my research. They turn what I say into what I type. They are calculators for words, and a good calculator is a gift.

The tools are real. The hype is the problem. And the hype has crawled out of the product and into your portfolio.

The Teardown

1. The Word Is Doing Work the Word Cannot Do

The term “AI” gets thrown around as though a mind has been born in a server farm. It has not. What exists is a class of remarkable instruments, useful the way a printing press was useful, the way a spreadsheet was useful. Instruments do not justify forty percent of a nation’s invested wealth. Stories do. And a story is exactly what is being sold to you, dressed in the language of inevitability so you will not think to ask the boring questions a steward is supposed to ask.

2. The Concentration Is the Crisis

Sløk’s point is not that these companies are bad. Some are extraordinary. His point is structural. When ten names carry forty percent of the index, the index stops protecting you. The whole reason a man buys broadly is so that no single failure can take his house down with it. That protection has quietly evaporated, and almost no one told the men holding the funds. A sharp drop in the leaders, Apollo warns, could erase years of gains in weeks.

3. The Velocity Should Make You Sober, Not Excited

Consider one company in this race. It raised money at a valuation near nine hundred sixty-five billion dollars, then filed to go public days later. I will be honest with you, some of the tools I praised a moment ago come from that very company, so I have no interest in dressing this up or tearing it down unfairly. I am not predicting its failure. I am pointing at the speed.

The culture has built a machine that can manufacture a near-trillion-dollar valuation faster than a young couple can save a down payment on a starter home. Ask yourself, soberly, what kind of thing appreciates that fast, and whether the thing you are building for your children is supposed to keep pace with it.

4. The Noise Is Engineered

Jim Cramer points at the screen.

The hype is pushed in your feeds.

The cable desk runs the ticker in red and green to keep your pulse up.

None of this is built to make you wise. It is built to make you trade, because your trading is how they eat.

The financial noise is the same machine as every other machine pulling at a modern man, dressed in a suit and given a stock symbol.

It wants your attention and your hard-earned dollars, and it does not pray for you.

The Spiritual Cost

There is a parable about a man exactly like the one the market is counting on. His land produced abundantly, and he had a problem most men would envy: too much to store. So he made a plan. He would tear down his barns and build bigger ones, and then he would say to his soul, take your ease, eat, drink, be merry.

“But God said unto him, Thou fool, this night thy soul shall be required of thee: then whose shall those things be, which thou hast provided?” (Luke 12:20)

Don’t get confused and think he was condemned for being rich. He was condemned for building his whole security on a harvest, and forgetting that the harvest was never the point. The market is asking you to be that man. To build your barns on one season’s narrative and call it a foundation.

Our Lord finished the lesson with the verse that should be carved over every brokerage door. “For where your treasure is, there will your heart be also.” (Luke 12:34) I have spent a career watching men store their treasure in things the grave empties, and watched their hearts go right into the vault with it.

The Pivot You Cannot Forget

Here is the thing you will not be able to forget once you have read it.

The index was never diversification. It was the feeling of diversification, and the feeling lasted exactly as long as the story did. The moment you understand that forty percent of the market is one bet wearing the costume of five hundred, you cannot go back to pretending your retirement is safe because a man on television used the word passive.

And the deeper cut is this: The same culture that built this fragile tower is the culture that taught you to measure a man’s life the way it measures a stock. By its velocity. By how fast it appreciated. By the number at the top of the statement. That is the single point of failure that should actually scare you, because a life built on that metric fails the same way the index does. All at once, when the story breaks, with nothing underneath.

The Real Path in 7 Small Steps

I wrote Five Principles because men kept asking me how to think about money without losing their souls to it. The details will follow, because it is the answer to everything above.

None of this is a recommendation to buy or sell any particular thing. It is the framework a steward thinks with taken from deep study of the greatest financial minds of all time.

What you do inside this advice is between you, your wife, and a fiduciary who is legally bound to you and not to a sales desk.

#1 Wealth Is Not Money

Money is a tool. Wealth is what is left when the tool is gone: a marriage that held, children who can stand, a faith that does not depend on the market being green.

Practically, this means you stop measuring yourself by the number at the top of the brokerage statement and start measuring by a harder question. If my income stopped tomorrow, how long could my household stand? It’s a question about time, your time, your life. How long you last. Most men have never run that number, because the number is frightening. Run it anyway.

A man who knows exactly how many months his family can survive a layoff is wealthier, in every way that matters, than a man with a bigger balance who has never asked.

#2 Build the Wall Before You Build the Tower

Before a single dollar goes into any market, you need a wall around your household. The Fed’s own survey found that thirty-seven percent of American adults could not cover a four-hundred-dollar emergency with cash.

More than a third of this country is one transmission, one ER visit, one broken furnace away from a credit card they cannot pay off.

This is a survival problem, and you solve it first, in this order.

A starter emergency fund. A couple thousand in a boring savings account you do not touch. A circuit breaker, so the next minor disaster does not become debt.

Kill the consumer debt. Every card, every note, one at a time, with everything you can throw at it. Dave Ramesy recommends smallest to largest; it’s sound advice.

Debt is the one position guaranteed to compound against you. You will never out-invest a credit card charging you twenty-four percent. Pay it off and you have earned a guaranteed twenty-four percent return, which no fund on earth can promise you.

Three to six months of real expenses, in cash, untouched. This is the moat. This is the thing that lets you keep your head when the market is on fire and every other man is selling at the bottom to make rent.

The men who get rich in a crash are simply the men who did not have to sell during one.

Boring? Completely. Boring is the point. The boring wall is what makes the interesting building possible.

#3 Stewardship Is Taught Generationally

Seventy percent of family wealth is gone by the second generation, ninety percent by the third. Because the formation of the family was too small, not the balance you left them. Realize you are not building a balance for your children. You are building men and women who know what to do with one.

In this way, whether you leave nothing financial behind or $5,000 or $5,000,000 your children will know what to do with it.

The practical work is not hiding the money in a trust and hoping. It is bringing your children inside the machine while they are young. Let them watch you say no to something you could afford. Let them see the giving happen before the spending. Give a teenager a small sum and the dignity of losing some of it on a bad decision while the stakes are survivable, because a man who first loses money at fifty with his retirement on the line is a man who was never taught.

The inheritance that lasts is because one has the competence to handle it.

#4 Financial Success Only Happens on Purpose

No man drifts into a legacy. The market drifts. You must not.

This is where you write the boring document almost no household has: a plan on paper. What comes in, what goes out, what gets stored, what gets given, decided in advance and in writing, when you are calm, so that the decision is already made before the salesman, the screen, or the panic ever reaches you.

The famous investor, Benjamin Graham, drew the line between an investor and a speculator right here.

The investor decides his rules in the cold light of reason and follows them when his blood is up. The speculator reacts to the screen. One of those men builds a legacy. The other funds the casino. The difference is not intelligence or income. It is whether the decision was made on purpose, ahead of time, or in the heat of a market doing what markets do.

#5 Debt Is Dangerous

It is the leash the modern economy hands you and calls a tool. A man who owes is a man who can be moved.

Here is the rule a steward lives by: the only acceptable debt is debt that cannot bankrupt you and that is buying something which will still exist when the note is paid.

A modest mortgage on a home you can afford even if your income drops, perhaps.

The car loan you signed to feel successful, the cards you carry to fund a life you have not yet earned, the line of credit that lets you skip the discipline of waiting, those are not tools. Those are how the system turns a free man into a renter of his own life.

The philosopher Nassim Taleb’s whole warning fits in one line: a man who is leveraged has handed someone else the timing of his ruin.

The unleveraged man may grow slower, but he cannot be forced to sell at the bottom, cannot be margin-called the week he loses his job, cannot be wiped out by a single bad season. He is harder to kill. In a fragile economy, that is the entire game.

#6 Invest Broadly, and Read the Room

When the market is greedy, be careful. When the market is crashing, be aggressive. Right now the market is greedy, and it is greedy about one thing. A steward notices that.

Broadly means broadly. Not the index pretending to be five hundred companies while ten of them carry forty percent of the weight. Truly broad ownership reaches past the story the whole country is buying at once: smaller companies, foreign companies, boring companies that make boring things people will still need when the narrative breaks, and yes, the productive assets and hard things that do not depend on any single quarter’s hype.

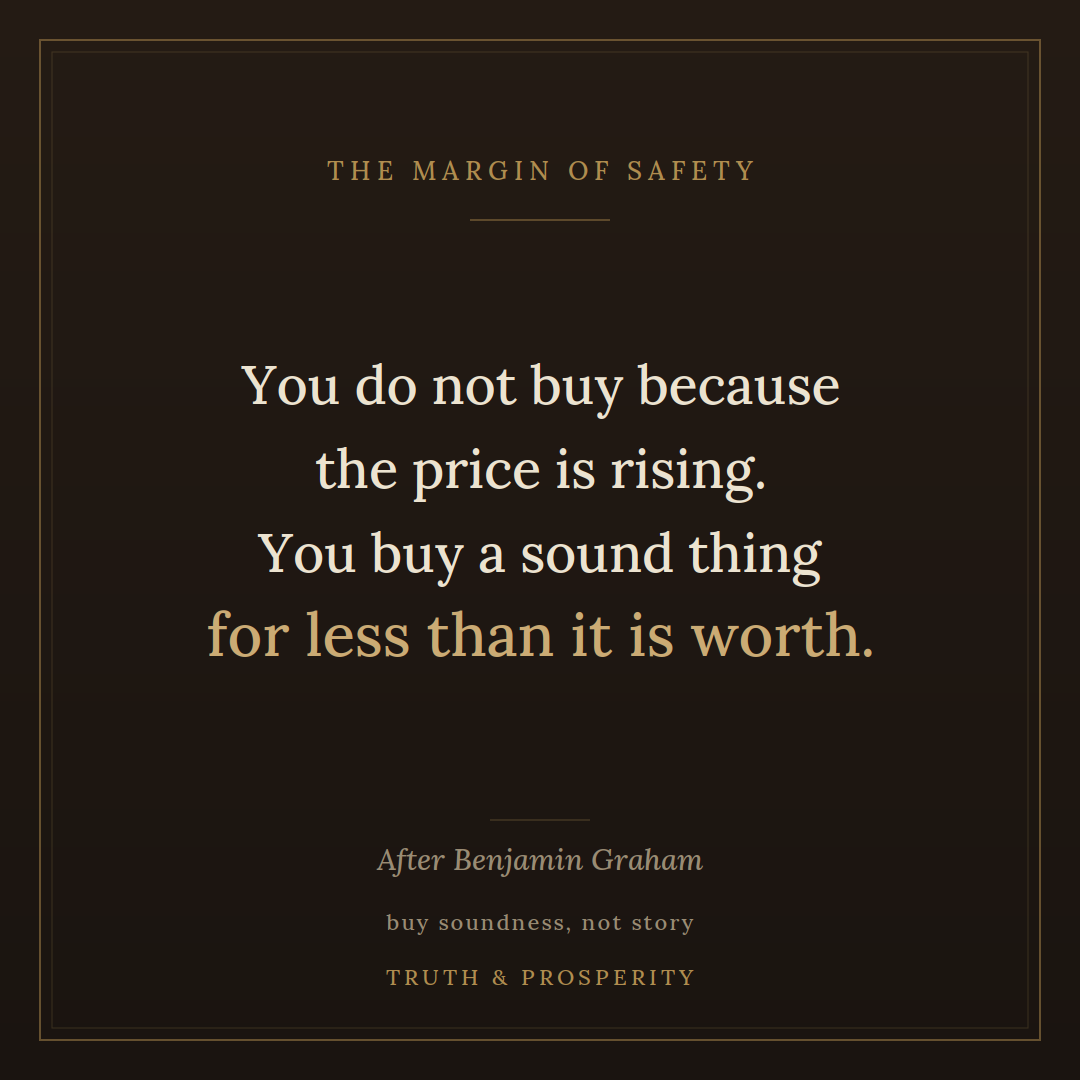

You do not buy because the price is rising and the story is exciting. You buy a sound thing for less than it is worth, so that even if you are wrong, you are protected. This is Graham’s famous margin of safety, buy for less than it’s worth.

The crowd does the opposite. It pays the most for the story exactly when the story is loudest, which is exactly when the margin of safety is gone, or inverse. When everyone you know is certain about the same two letters, that is not the time to follow. That is the time a steward gets careful.

#7 Invest in What Will Outlast You

Find the things that compounds longest.

This is Taleb’s deepest point: survival comes first, because you cannot compound if you are wiped out. A return of forty percent followed by a total loss is not a forty percent gain. It is a zero. The man who never blows up, who keeps a wall of cash, who refuses leverage, who owns broadly and patiently, will quietly pass the man chasing the hot thing, because the hot man eventually meets the season he will not survive.

Slow and unkillable beats fast and fragile over a lifetime, every single time.

But the truest holdings on this list never traded on any exchange. A child discipled. A wife known. A faith handed down intact. A church funded. A name that means something at the graveside. These are the only positions the grave cannot mark down, and they compound in the one account that does not close when your heart stops.

The Line in the Sand

The men managing the index made their bet. You do not have to make the same one with your one short life.

Build broadly with your money, soberly, like a man who has read the warnings. But build your self on the only foundation that has never had a bad quarter in two thousand years. One of these will be required of you, suddenly, on a night you did not schedule. The other will still be standing.

The market built a single point of failure. A steward builds something that cannot fail all at once, because it was never resting on a story to begin with.

That is how you build a legacy death cannot take.

If this resonated, you belong here. Truth & Prosperity is a weekly letter for men building lives the world cannot bend. Faith, family, finance, legacy.

Subscribers get the Legacy Audit free in their email, twelve questions, including three stewardship questions that cut straight to whether you are building for a harvest that will never come or on a foundation death cannot take.

Subscribe free, and let us build something that outlives us.

Great article !!